The closest thing we have in this country to Medicare for all, of course, is Medicare. So how do people on Medicare rate their healthcare coverage and care?

In a November 2018 Gallup Poll on satisfaction with coverage and care, seniors and Medicaid/Medicare recipients rated their coverage and the healthcare care most positively among all group groups, with 9 in 10 seniors rating both positively.

For all adults covered by Medicare/Medicaid, 79 percent rated their healthcare coverage as excellent or good, compared to 70 percent for privately insured adults. On the other hand, 85 percent of adults covered by private insurance rated the healthcare they receive as excellent or good, compared to 79 percent for Medicare/Medicaid recipients. As might be expected, many more Medicare/Medicaid recipients are more satisfied with the costs they pay (70 percent vs. 51 percent) than those covered with private insurance (McCarthy, 2018).

It is interesting to note that the Gallup survey found that Americans are more satisfied with the personal costs they pay for health care than they are with the total national costs of healthcare. Since 2001, this survey has found that satisfaction with personal costs has ranged from 54 percent to 58 percent, while satisfaction with the total cost of healthcare in the United States has averaged 21 percent (20 percent in the latest survey). According to the study summary, “While Americans are more likely to be satisfied than dissatisfied with their own costs, they tend to see the overall U.S. healthcare system as overly expensive for others.”

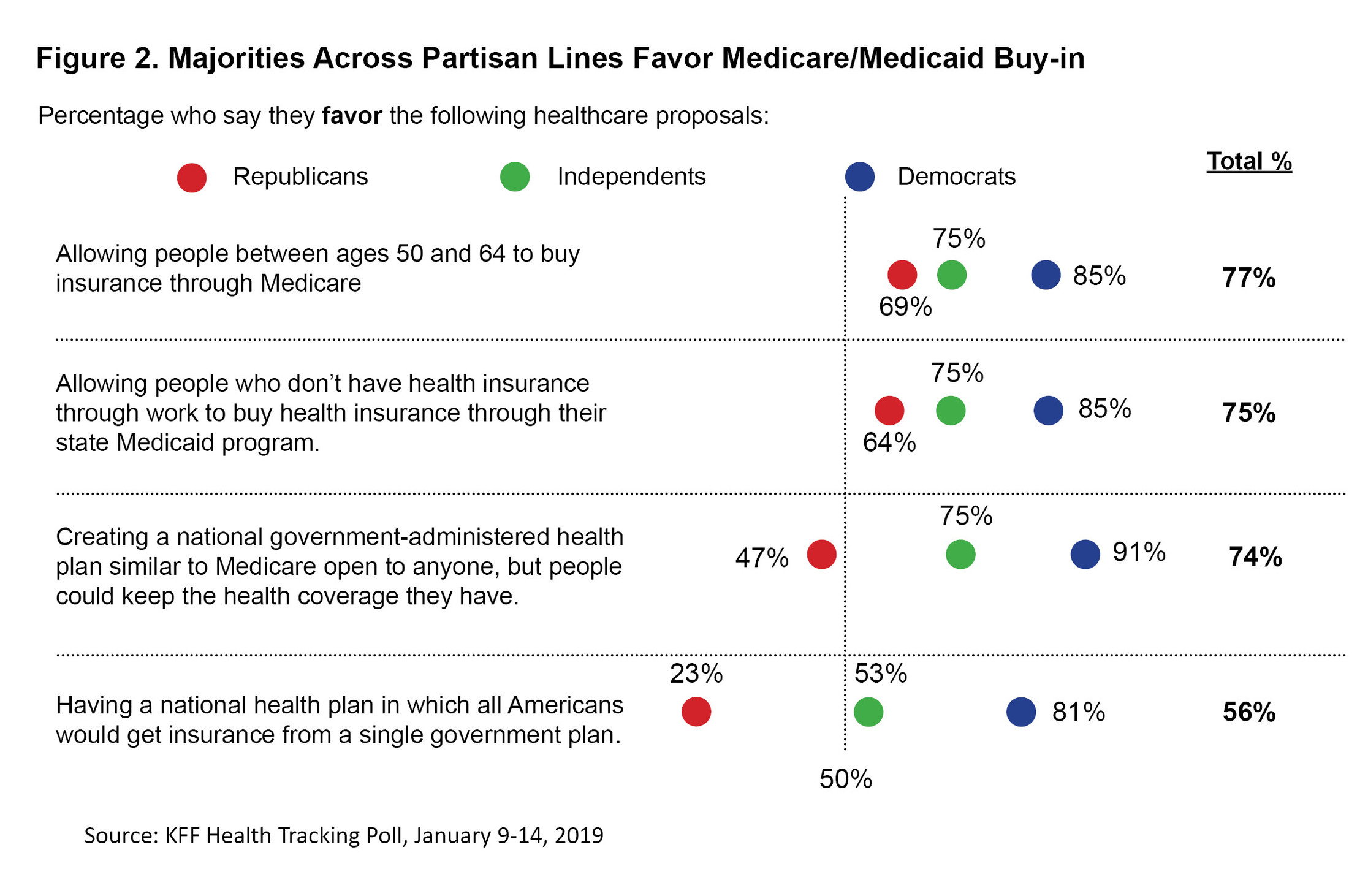

The new year brought fresh debate over single-payer healthcare, as Democratic presidential challengers began hitting the campaign trail. It will be interesting to see whether the new bill in the House contains major departures from the Senate version, and whether that bill—and the individual platforms of the Democratic candidates—will move more toward some of those middle-of-the-road Medicare buy-in options mentioned earlier from the Kaiser study.

Still, single-payer healthcare does check many of the desired boxes for consumers, including cost and the improved care and attention they could potentially receive from providers. On the other hand, people generally seem to want to hold onto the plans they have, and those who might be enthusiastic at the prospect of coverage for everyone will have to weigh that against the tax bite.

In our next and last hypothetical consumer-oriented model, we take a 180-degree spin around to explore the private health insurance model.

References

Frankel, R. S. (2017, June 7). Worried sick about your health care? You’re not alone. Blog post. Bankrate. Retrieved from https://www.bankrate.com/banking/savings/money-pulse-0617/

Luhby, T., & Krieg, G. (2019, January 29). Harris backs ‘Medicare-for-all’ and eliminating private insurance as we know it. CNN. Retrieved from: https://www.cnn.com/2019/01/29/politics/harris-private-insurance-medicare/index.html

McCarthy, J. (2018, December 7). Most Americans still rate their healthcare quite positively. Gallup. Accessed at: https://news.gallup.com/poll/245195/americans-rate-healthcare-quite-positively.aspx

Pew Research. (2018). Pew Research Center September 2018 political survey: Final topline September 18-24, 2018. Retrieved from http://www.pewresearch.org/wp-content/uploads/2018/10/FT_18.10.03_HealthCare_Topline.pdf

Kirzinger, A., Muñana, C. & Brodie, M. (2019, January 23). Kirzinger, A., Muñana, C. & Brodie, M. (2019, January 23). KFF Health Tracking Poll–January 2019: The Public on next steps for the ACA and proposals to expand coverage. Kaiser Family Foundation. Retrieved at: https://www.kff.org/health-reform/poll-finding/kff-health-tracking-poll-january-2019